United Kingdom (UK) SME Insurance Market Size, Trends, Competitor Dynamics and Opportunities

Powered by ![]()

All the vital news, analysis, and commentary curated by our industry experts.

United Kingdom (UK) SME Insurance Market Report Overview

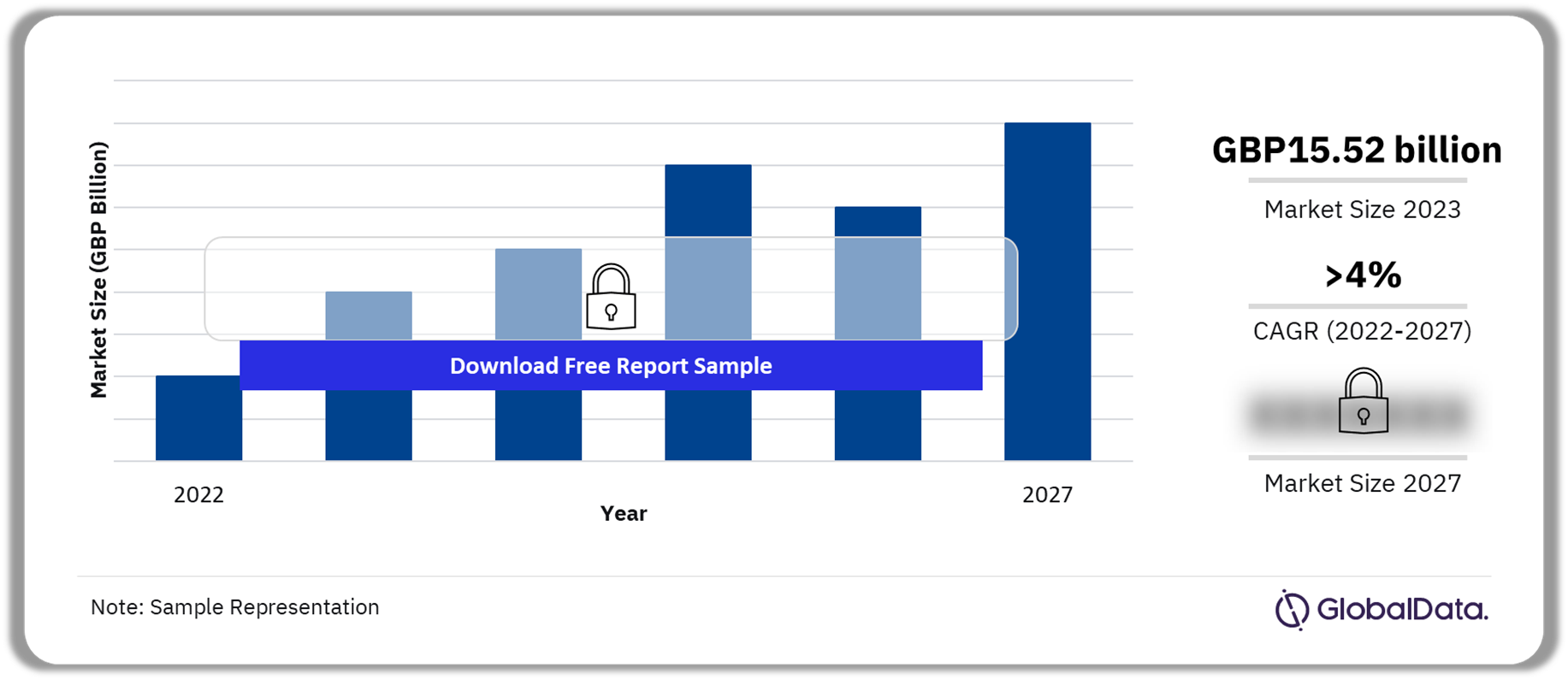

The UK SME insurance market generated gross written premiums (GWP) worth GBP15.52 billion in 2023. The primary factor contributing to GWP growth in 2023 was a large year-round hardening of premiums. The rise in claims expenses, which were often passed on to customers, also contributed to the overall increase in GWP. Various insurance categories witnessed substantial increases in the cost of coverage, primarily due to inflationary pressures and challenges in the global supply chain. However, insurers responded by adjusting premiums to account for these elevated costs. The GWP in the UK SME insurance market will grow at a CAGR of more than 4% from 2022 to 2027.

UK SME Insurance Market Outlook 2022-2027 (GBP Billion)

Buy the Full Report for Additional Insights on the UK SME Insurance Market Forecasts, Download a Free Sample Report

The UK SME insurance market research report offers insights into the significance of SMEs within the commercial insurance market and how they are influenced by the UK economy. The report enables clients to identify the effects of the cost-of-living crisis on the UK SME insurance space. Furthermore, the UK SME insurance report outlook presents growth opportunities in the SME space as well as challenges faced by SMEs.

| Market Size (2023) | GBP15.52 billion |

| CAGR (2022-2027) | >4% |

| Key Concerns | · Cost-of-living Crisis

· Incoming/Possible Recession · High Interest/Borrowing Costs · Increase in Business Rates · Cyber Crime |

| Key SMEs by Size | · Medium

· Small · Micro · Sole Trader |

| Key Insurance Products | · Employers’ Liability Insurance

· Public Liability Insurance · Professional Indemnity Insurance · Property Insurance · Cyber Insurance |

| Enquire & Decide | Discover the perfect solution for your business needs. Enquire now and let us help you make an informed decision before making a purchase. |

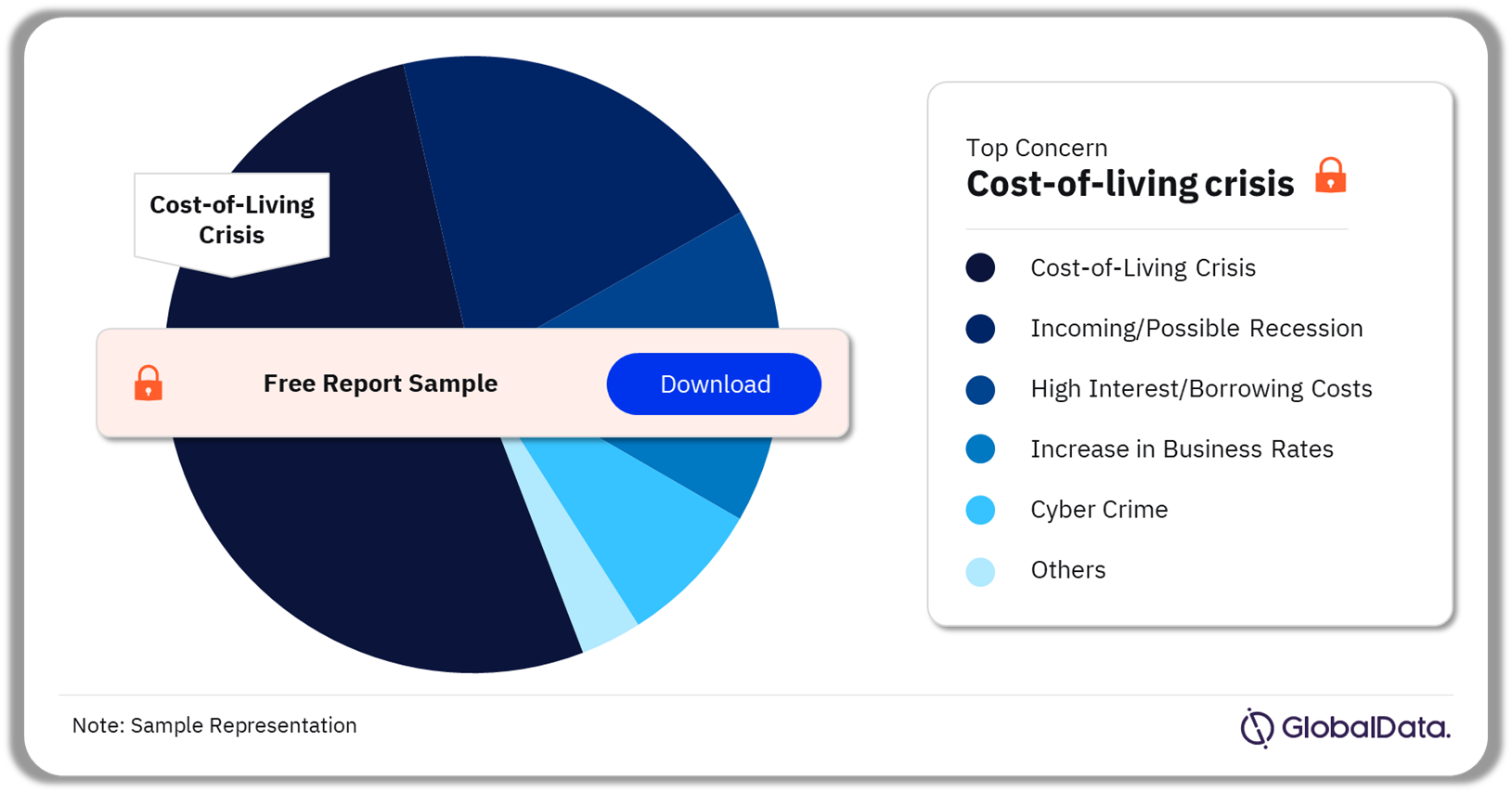

UK SME Insurance Market Segmentation by Key Concerns

Cost-of-living crisis, incoming/possible recession, high interest/borrowing costs, increase in business rates, and cyber crime are a few of the key reasons for concern among SME insurers. In 2023, the cost-of-living crisis was the topmost concern raised by the SMEs. This heightened level of concern reflects the significant impact of the cost-of-living crisis on the business environment. The seriousness of this concern corresponds with the widespread challenges businesses encounter, encompassing rising operational costs and potential effects on consumer spending.

UK SME Insurance Market Analysis by Key Concerns, 2023 (%)

Buy the Full Report for More Insights on the Key Concerns Highlighted in the UK SME Insurance Market, Download a Free Sample Report

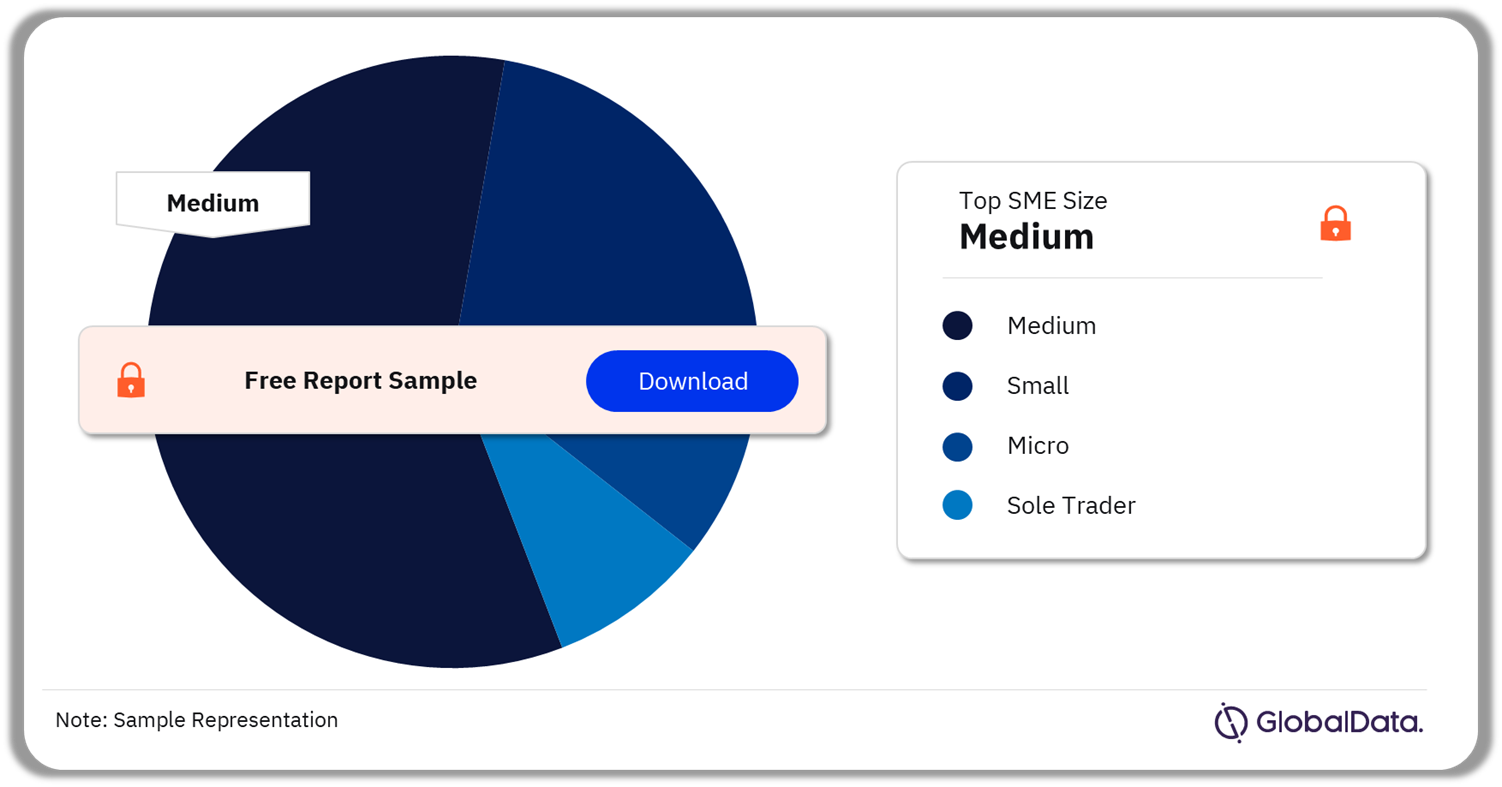

UK SME Insurance Market Segmentation by SME Size

The UK SME insurance product landscape comprises a significant component, namely, packaged insurance plans. These are plans wherein several insurance policies are purchased from the same insurer or broker. The key SMEs are classified by size into medium, small, micro, and sole trader. In 2023, medium-sized enterprises was the leading SME size that purchased insurance via a package. Bundled insurance packages offer a streamlined and simplified solution for businesses, consolidating multiple policies under a single umbrella.

UK SME Insurance Market Analysis by SME Size, 2023 (%)

Buy the Full Report for More Insights on the SME Size in the UK SME Insurance Market, Download a Free Sample Report

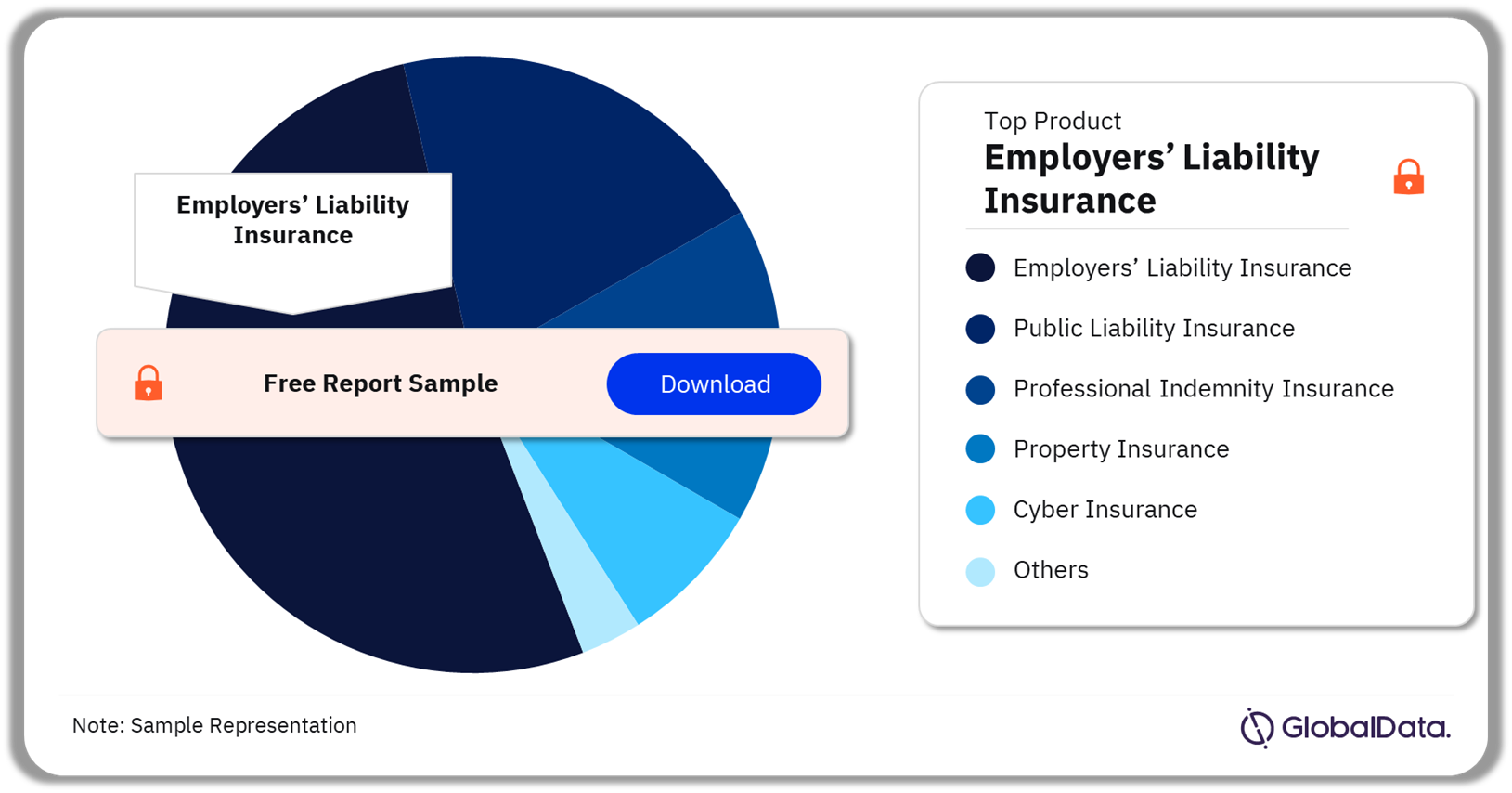

UK SME Insurance Market Segmentation by Products

The key products in the UK SME insurance market are employers’ liability insurance, public liability insurance, professional indemnity insurance, property insurance, and cyber insurance among others. In 2023, employers’ liability insurance saw the biggest growth. As business operations resumed and employees returned to workplaces, companies likely recognized the heightened importance of ensuring comprehensive coverage for workplace-related risks.

UK SME Insurance Market Analysis by Products, 2023 (%)

Buy the Full Report for More Product-Wise Insights into the UK SME Insurance Market, Download a Free Sample Report

Key Segments Covered in this Report

UK SME Insurance Concern Outlook, (%, 2023)

- Cost-of-living Crisis

- Incoming/Possible Recession

- High Interest/Borrowing Costs

- Increase in Business Rates

- Cyber Crime

UK SME Insurance SME Size Outlook (%, 2023)

- Medium

- Small

- Micro

- Sole Trader

UK SME Insurance Product Outlook (%, 2023)

- Employers’ Liability Insurance

- Public Liability Insurance

- Professional Indemnity Insurance

- Property Insurance

- Cyber Insurance

Scope

• The number of SMEs in the UK increased by 0.8% in 2023, rising from 5,501,260 to 5,547,170.

• The cost-of-living crisis is SMEs’ biggest concern, with 81.8% of SMEs concerned to some degree.

• The SME insurance market is set to be worth GBP15.52 billion in 2023e, up 11.2% on 2022.

• GlobalData forecasts the SME insurance market to reach GBP17.32 billion in 2027, recording a compound annual growth rate (CAGR) of 4.4% over 2022–27.

Key Highlights

- Learn about the significance of SMEs within the commercial insurance market and how they are influenced by the UK economy.

- Identify the effects of the cost-of-living crisis on the UK SME insurance space.

- Discover GlobalData’s forecasts for the market.

- Recognize the challenges faced by UK SMEs.

- Identify growth opportunities in the SME market.

Reasons to Buy

• Learn about the significance of SMEs within the commercial insurance market and how they are influenced by the UK economy.

• Identify the effects of the cost-of-living crisis on the UK SME insurance space, as well as other challenges faced by SMEs.

• Discover GlobalData’s forecasts for the SME insurance market.

• Identify growth opportunities in the SME space.

Society of Motor Manufacturers and Traders

Department for Work and Pensions

Acturis

JUMPSEC

Table of Contents

Table

Figures

Frequently asked questions

-

What was the UK SME insurance market size in 2023?

The UK SME insurance market generated gross written premiums (GWP) worth GBP15.52 billion in 2023.

-

What will the CAGR growth rate of the UK SME insurance market be during 2022-2027?

The GWP in the UK SME insurance market will grow at a CAGR of more than 4% from 2022 to 2027.

-

Which was the topmost concern in the UK SME insurance market in 2023?

In 2023, the cost-of-living crisis was the topmost concern raised by the SMEs.

-

Which was the leading product in the UK SME insurance market in 2023?

In 2023, employers’ liability insurance saw the biggest growth.

Get in touch to find out about multi-purchase discounts

reportstore@globaldata.com

Tel +44 20 7947 2745

Every customer’s requirement is unique. With over 220,000 construction projects tracked, we can create a tailored dataset for you based on the types of projects you are looking for. Please get in touch with your specific requirements and we can send you a quote.

Sample Report

United Kingdom (UK) SME Insurance Market Size, Trends, Competitor Dynamics and Opportunities was curated by the best experts in the industry and we are confident about its unique quality. However, we want you to make the most beneficial decision for your business, so we offer free sample pages to help you:

- Assess the relevance of the report

- Evaluate the quality of the report

- Justify the cost

Download your copy of the sample report and make an informed decision about whether the full report will provide you with the insights and information you need.

Related reports

View more Non-Life Insurance reports