United Kingdom (UK) Commercial Motor Insurance Market Trends, Competitor Dynamics and Opportunities

Powered by ![]()

All the vital news, analysis, and commentary curated by our industry experts.

The gross written premium (GWP) in the UK commercial motor insurance market was valued at GBP5.65 billion in 2022. The UK commercial motor insurance market experienced a marginal decline of 0.3% in gross written premiums (GWP) in 2022 when compared to the preceding year. However, a sharp rise in premiums throughout 2023 will cause significant growth in the market. According to GlobalData forecasts, the UK commercial motor insurance market will bounce back in 2023, driven by soaring premiums due to rising claims costs, and is expected to record a CAGR of more than 4% from 2022 to 2027.

UK Commercial Motor Insurance Market Outlook 2022-2027 (GBP Billion)

Buy The Full Report for More Information on The UK Commercial Motor Insurance Market Forecast, Download A Free Report Sample

The UK commercial motor insurance market research report offers insights into the motor insurance scenario within the commercial insurance market and how it is influenced by volatility in the economy. It also ascertains how newcomers and insurtechs are disrupting and driving innovation in the country’s insurance industry. The report enables clients to identify the effects of the cost-of-living crisis on the UK commercial motor insurance space. Furthermore, the report’s outlook presents growth opportunities in the motor insurance space as well as challenges faced by the insurance providers.

| GWP (2022) | GBP5.65 billion |

| CAGR (2022-2027) | >4% |

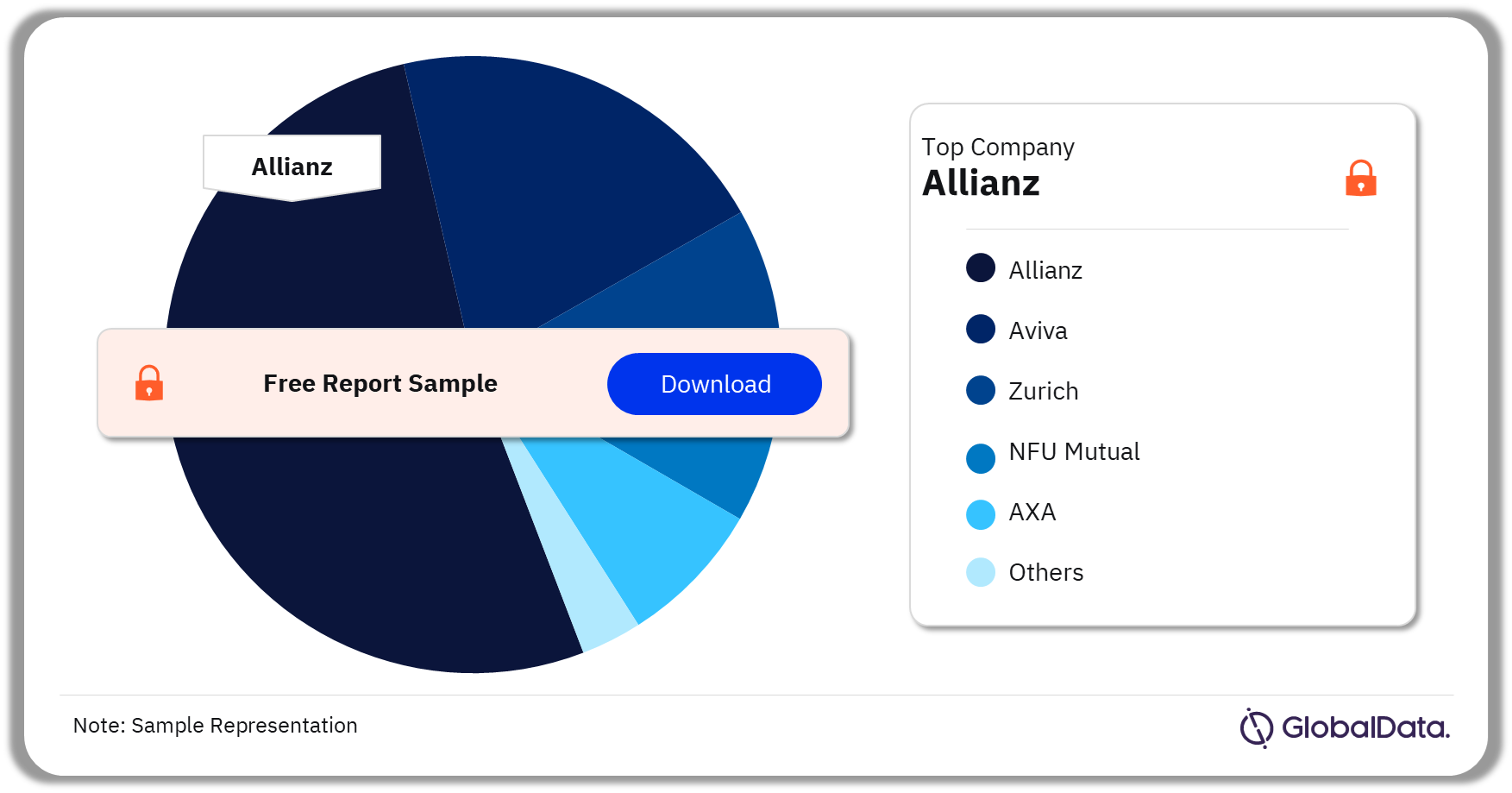

| Key Players | · Allianz

· Aviva · Zurich · NFU Mutual · AXA |

| Enquire & Decide | Discover the perfect solution for your business needs. Enquire now and let us help you make an informed decision before making a purchase. |

UK Commercial Motor Insurance Market Dynamics

The UK commercial motor insurance GWP decreased by 0.3% in 2022, a noticeable contrast to the robust growth seen in 2021. Economic challenges, driven by rising inflation and heightened uncertainty, prompted businesses to re-evaluate their operations and insurance needs. Some companies have responded to these financial challenges by adjusting their budgets, which has affected their spending on commercial motor insurance.

In addition, a decline in the penetration rates of SMEs purchasing commercial insurance, specifically in commercial fleet and single van insurance, from 2021 to 2022 also hindered the commercial motor insurance market growth. However, sharp rises in premiums throughout 2023 caused significant growth in the market. The UK commercial motor insurance market is estimated to grow by 19.4% in 2023, driven by record-breaking increases in premiums as the cost of claims continues to rise.

Furthermore, the total number of commercial vehicles registered in the UK increased by 3.1% from 2021 to 2022. Likewise, the number of light goods vehicles (LGVs) and heavy goods vehicles (HGVs) increased by 1.8% and 1.5%, respectively during the same period. This surge can be attributed to the COVID-19 pandemic, which led to a substantial rise in e-commerce and home deliveries. On the other hand, the number of licensed buses and coaches in the UK decreased by 2.1% from 2021 to 2022. This again can be attributed to the COVID-19-induced travel restrictions.

The cost-of-living crisis in the UK is one of the most pressing challenges for businesses operating fleets. The rising cost of fuel, which is directly linked to inflation, strains their budgets, and affects overall profitability. The need to allocate more financial resources to fuel expenses poses a considerable financial burden on businesses with extensive fleets.

UK Commercial Motor Insurance Market – Growth Opportunities

The adoption of advanced technologies such as telematics, dashcams, and artificial intelligence (AI) is poised to reshape the commercial motor insurance landscape in the UK. For instance, telematics systems can lower costs and enhance personalization by providing in-depth insights into fleet operations, real-time monitoring of vehicle usage, fuel consumption, maintenance needs, and driver behavior. This data empowers businesses to optimize routes, reduce insurance costs, and enhance operational efficiency. Furthermore, telematics can improve fleet safety programs, promoting responsible driving behavior among employees.

Likewise, dashcams have emerged as a valuable tool in the realm of motor insurance, offering numerous advantages to both individuals and businesses. Dashcams can capture the driver’s perspective of the road, serving as a credible source of evidence in insurance claims. This evidence can expedite the claims process and enhance its accuracy, ultimately resulting in quicker resolutions and reduced operational costs for insurers.

Additionally, the rise in electric vehicles and autonomous vehicles in the commercial landscape will boost the motor insurance sector in the country. Commercial insurers must adapt to this shift by offering specialized insurance products. For instance, EV insurance policies should cover the unique risk factors associated with the vehicle, such as battery damage and repair costs. Insurers can also incentivize the adoption of EVs by offering discounts and coverage options tailored to businesses that prioritize sustainability. Similarly, the UK government’s plan to introduce self-driving vehicles on public roads by 2025 necessitates substantial regulatory changes and innovation within the insurance industry. The evolution of self-driving cars will significantly impact insurance costs, road safety, businesses, and commercial motor insurance as the technology matures and becomes increasingly integrated into everyday life. The commercial motor insurance sector must be adaptable to these transformative shifts, ensuring that businesses and fleets are adequately covered while managing the evolving risks associated with autonomous vehicles.

UK Commercial Motor Insurance Market – Competitive Landscape

A few of the leading insurers operating in the UK commercial motor insurance market are Aviva, Allianz, Admiral, Zurich, AXA, and NFU Mutual, among others. In 2022, Allianz overtook Aviva to become the leader in the UK commercial motor insurance market. Zurich remained in third position followed by NFU Mutual and AXA.

UK Commercial Motor Insurance Market Analysis, by Key Players

Buy The Full Report For More Insights On The UK Commercial Motor Insurance Market Players, Download A Free Report Sample

Scope

• The commercial motor insurance market is expected to grow by 19.4% in 2023e, following a 0.3% decrease in 2022.

• The total number of commercial vehicles increased by 3.1% in 2022.

• The total miles driven by all vehicles increased by 8.8% from 2021 to 2022.

• Gross claims incurred increased by 9.0% in 2022, while net claims incurred increased by 15.2%.

Key Highlights

- The commercial motor insurance market grew in 2021, reaching GBP5.5 billion in GWP.

- The total number of commercial vehicles on UK roads increased in 2021.

- The number of claims recorded fell in 2021, despite the increased number of vehicles on UK roads.

- Aviva remains the market leader.

Reasons to Buy

- Understand how COVID-19 and other factors have affected commercial motor insurance.

- Determine how the market leaders have maintained their position and evolved their product offerings in the past year.

- Understand the effects of the cost-of-living crisis.

- Ascertain how newcomers and insurtechs are disrupting and driving innovation.

- Identify areas for growth and development in the market going forward.

- Recognize the short-term and long-term challenges facing commercial motor insurers.

Aviva

Direct Line

Zurich

NFU Mutual

QBE

Humn.ai

AXA

RSA

QIC

Haven

LV=

ElectriX

Zego

Friss

Ageas

Churchill

Ezoo

Drive Fuze

Flock

Bikmo

Blike

Uber

Deliveroo

Stuart

WTW

Confused.com

Amazon

Tesla

Asda

Wayve

Table of Contents

Table

Figures

Frequently asked questions

-

What is the UK commercial motor insurance GWP in 2022?

The UK commercial motor insurance GWP was valued at GBP5.65 billion in 2022.

-

What is the expected UK commercial motor insurance market growth rate for the forecast period?

The UK commercial motor insurance market is expected to grow at a CAGR of more than 4% during 2022-2027.

-

Which are the key players in the UK commercial motor insurance market?

A few of the leading insurers operating in the UK commercial motor insurance market are Aviva, Allianz, Admiral, Zurich, AXA, and NFU Mutual, among others.

-

Which player leads in the UK commercial motor insurance market?

Allianz accounted for the highest share of the UK commercial motor insurance market in 2022.

Get in touch to find out about multi-purchase discounts

reportstore@globaldata.com

Tel +44 20 7947 2745

Every customer’s requirement is unique. With over 220,000 construction projects tracked, we can create a tailored dataset for you based on the types of projects you are looking for. Please get in touch with your specific requirements and we can send you a quote.

Sample Report

United Kingdom (UK) Commercial Motor Insurance Market Trends, Competitor Dynamics and Opportunities was curated by the best experts in the industry and we are confident about its unique quality. However, we want you to make the most beneficial decision for your business, so we offer free sample pages to help you:

- Assess the relevance of the report

- Evaluate the quality of the report

- Justify the cost

Download your copy of the sample report and make an informed decision about whether the full report will provide you with the insights and information you need.

Related reports

View more Motor reports