Personalization in Insurance – Thematic Intelligence

Powered by ![]()

All the vital news, analysis, and commentary curated by our industry experts.

Personalization in Insurance Thematic Report Overview

Insurance companies are recognizing the value of personalized policies to attract and retain customers. Insurers can personalize policies based on policyholder behaviors, preferences, and risk profiles, with unprecedented accuracy by leveraging AI and machine learning algorithms. Personalized policies not only provide customers with coverage that meets their specific requirements but also demonstrate an understanding of their unique circumstances, fostering trust and loyalty.

The ‘Personalization in Insurance’ thematic intelligence report gives you an in-depth insight into the personalization theme and the impact it will have on the insurance industry. It further entails a deep-dive analysis of the industry, including real-life use case studies that showcase how the insurance companies have responded to the impact of this theme on their operations. The report identifies the key market trends that will shape the personalization theme over the coming years and gives an insight into the market players and the competitive landscape within the theme.

| Report Pages | 69 |

| Regions Covered | Global |

| Value Chain | · Product Development

· Marketing and Distribution · Underwriting and Risk Profiling · Claims Management · Customer Service |

| Key Trends | · Technology Trends

· Macroeconomic Trends · Regulatory Trends |

| Leading Companies | · Admiral

· Allianz · Aviva · Bright Health Group · Bupa |

| Enquire & Decide | Discover the perfect solution for your business needs. Enquire now and let us help you make an informed decision before making a purchase. |

Personalization in Insurance – Key Trends

The primary trends that will shape the personalization theme over the next 12 to 24 months are classified into technology trends, macroeconomic trends, and regulatory trends.

- Technology trends: The key technology trends impacting the personalized theme are integration of advanced technologies such as artificial intelligence (AI), generative (AI), Internet of Things (IoT), and big data will have a profound impact on the personalization theme. Moreover, wearable tech, and the use of telematics to monitor and collect data allows insurers to personalize insurance policies based on a policyholder’s specific characteristics.

- Macroeconomic trends: Economic conditions characterized by high inflation, low consumer confidence, and elevated borrowing rates will significantly impact the personalization theme in the insurance industry. Additionally, changing demographics, climate and sustainability considerations, geopolitical issues, health trends, and generation rent are a few of the key macroeconomic trends expected to drive the market.

- Regulatory trends: Cybersecurity, data protection regulations, and AI regulation to address potential risks and ensure responsible deployment are part of the regulatory trends impacting the personalization in insurance theme.

Personalization in Insurance – Industry Analysis

Personalization in insurance for personal line products, including motor, home, travel, and pet insurance, involves tailoring coverage to meet the specific needs and preferences of individual policyholders. Insurers utilize various data points, ranging from simple to advanced, to gather insights into each customer’s unique risk profile, behaviors, and lifestyle.

Claims handling processes represent another critical area where personalization can make a difference. Insurers can streamline claims processing and tailor communication channels to suit individual preferences by leveraging advanced analytics and automation.

The personalization in insurance industry analysis also covers:

- The personal insurance markets

- The commercial insurance markets

- Life and health insurance

- Timeline

Personalization in Insurance Market, 2019-2030

Buy the Full Report for More Insights into Personalization in Insurance Market Forecasts

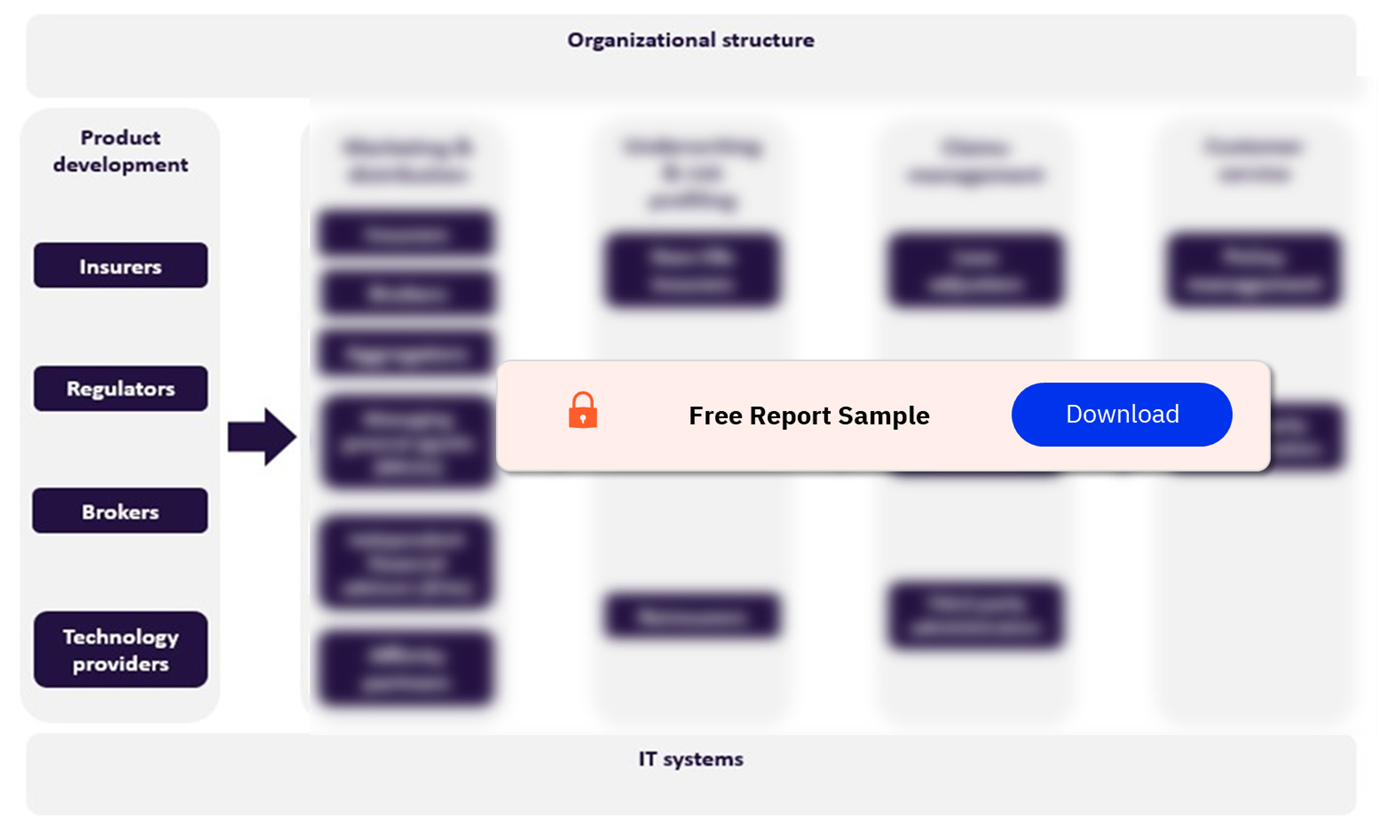

Personalization in Insurance - Value Chain Analysis

The personalized value chain consists of product development, marketing and distribution, underwriting and risk profiling, claims management, and customer service.

Product Development: Product development is a pivotal stage in the insurance value chain, and its significance is particularly pronounced in the context of the personalization theme within insurance. Insurers leverage this stage to create insurance products that align closely with the unique needs and preferences of individual policyholders.

Personalized insurance products crafted during the product development stage that not only enhance customer satisfaction but also contribute to improved risk assessment, pricing accuracy, and overall customer experience.

Insurance Industry Value Chain Analysis

Buy the Full Report for More Insights into the Insurance Industry Value Chain

Leading Companies

A few leading insurance companies making their mark within the personalized theme are:

- Admiral

- Allianz

- Aviva

- Bright Health Group

- Bupa

Admiral: In December 2023, Admiral announced that it had bought RSA’s UK direct home and pet personal lines insurance operations. Under the agreement, RSA will also transfer new business franchises, as well as certain operations, brands, data, renewal rights, and some 300 personnel, to Admiral.

Buy the Full Report to Know More about the Leading Companies in the Personalization Theme

Life Insurance Sector Scorecard

At GlobalData, we use a scorecard approach to predict tomorrow’s leading companies within each sector. Our power sector scorecard has three screens: A thematic screen, a valuation screen, and a risk screen.

- The thematic screen ranks companies based on overall leadership in the 10 themes that matter most to their industry, generating a leading indicator of future performance.

- The valuation screen ranks our universe of companies within a sector based on selected valuation metrics.

- The risk screen ranks companies within a particular sector based on overall investment risk.

- The personalization in insurance – thematic intelligence report also includes non-life insurance sector scorecard

Life Insurance Sector Scorecard – Thematic Screen

Buy the Full Report to Know More about the Life Insurance Sector Scorecards

Scope

• GlobalData’s 2023 UK Insurance Consumer Survey indicates that the cost of premiums is a primary concern for 34.2% of consumers.

• There is varying interest in usage-based insurance policies based on potential premium savings, with 16.8% interested if it saved them 10%.

• The primary motivation for homeowners to consider sharing data from smart home devices with a home insurance company is financial savings, with 70.4% of respondents selecting this option as per GlobalData’s 2023 UK Insurance Consumer Survey.

• According to GlobalData surveying, SMEs rank improved safety measures as the most important feature of usage-based insurance.

Key Highlights

- Scientific overview of personalization

- Studies of emerging technological trends and their broader impact on the market.

- Analysis of the various military and civilian hypersonic technologies programs currently under development, their history, and projections on future development initiatives.

Reasons to Buy

- Determine potential investment companies based on trend analysis and market projections.

- Gaining an understanding of the market challenges and opportunities surrounding the personalization theme.

- Understand how spending on personalization will fit into the overall market and which spending areas are being prioritized.

Farmers

Lemonade

Amica

Hippo

Blink

Sompo Holdings

AIA

Aviva

Admiral

Allianz

Bright Health Group

Bupa

Chubb

Cuvva

Dacadoo

DeadHappy

Descartes

Direct Line

Discovery

FloodFlash

Flock

GetSafe

Hiscox

Ladder

Marshmallow

Metromile

Next Insurance

Oscar Health

Ping An

Root

Tapoly

Tokio Marine

Tractable

Trov

Viatlity

Yu Life

Zego

Table of Contents

Frequently asked questions

-

What are the key technology trends that will impact the personalization theme in the insurance industry?

The key technology trends impacting the personalized theme are integration of advanced technologies such as artificial intelligence (AI), generative (AI), Internet of Things (IoT), and big data will have a profound impact on the personalization theme. Moreover, wearable tech, and the use of telematics to monitor and collect data allows insurers to personalize insurance policies based on a policyholder’s specific characteristics.

-

What are the key macroeconomic trends that will impact personalization theme in the insurance industry?

Economic conditions characterized by high inflation, low consumer confidence, and elevated borrowing rates will significantly impact the personalization theme in the insurance industry. Additionally, changing demographics, climate and sustainability considerations, geopolitical issues, health trends, and generation rent are a few of the key macroeconomic trends expected to drive the market.

-

What are the key regulatory trends that will impact personalization theme in the insurance industry?

Cybersecurity, data protection regulations, and AI regulation to address potential risks and ensure responsible deployment are part of the regulatory trends impacting the personalization in insurance theme.

-

What are the key components of the personalization value chain?

The key components of the personalization value chain are product development, marketing and distribution, underwriting and risk profiling, claims management, and customer service.

-

Which are the leading insurance companies associated with the personalization theme?

A few of the insurance companies making their mark in the personalization theme are Admiral, Allianz, Aviva, Bright Health Group, and Bupa among others.

Get in touch to find out about multi-purchase discounts

reportstore@globaldata.com

Tel +44 20 7947 2745

Every customer’s requirement is unique. With over 220,000 construction projects tracked, we can create a tailored dataset for you based on the types of projects you are looking for. Please get in touch with your specific requirements and we can send you a quote.

Sample Report

Personalization in Insurance – Thematic Intelligence was curated by the best experts in the industry and we are confident about its unique quality. However, we want you to make the most beneficial decision for your business, so we offer free sample pages to help you:

- Assess the relevance of the report

- Evaluate the quality of the report

- Justify the cost

Download your copy of the sample report and make an informed decision about whether the full report will provide you with the insights and information you need.

Related reports

View more Non-Life Insurance reports