United Kingdom (UK) Cards and Payments – Opportunities and Risks to 2027

Powered by ![]()

All the vital news, analysis, and commentary curated by our industry experts.

UK Cards and Payments Market Report Overview

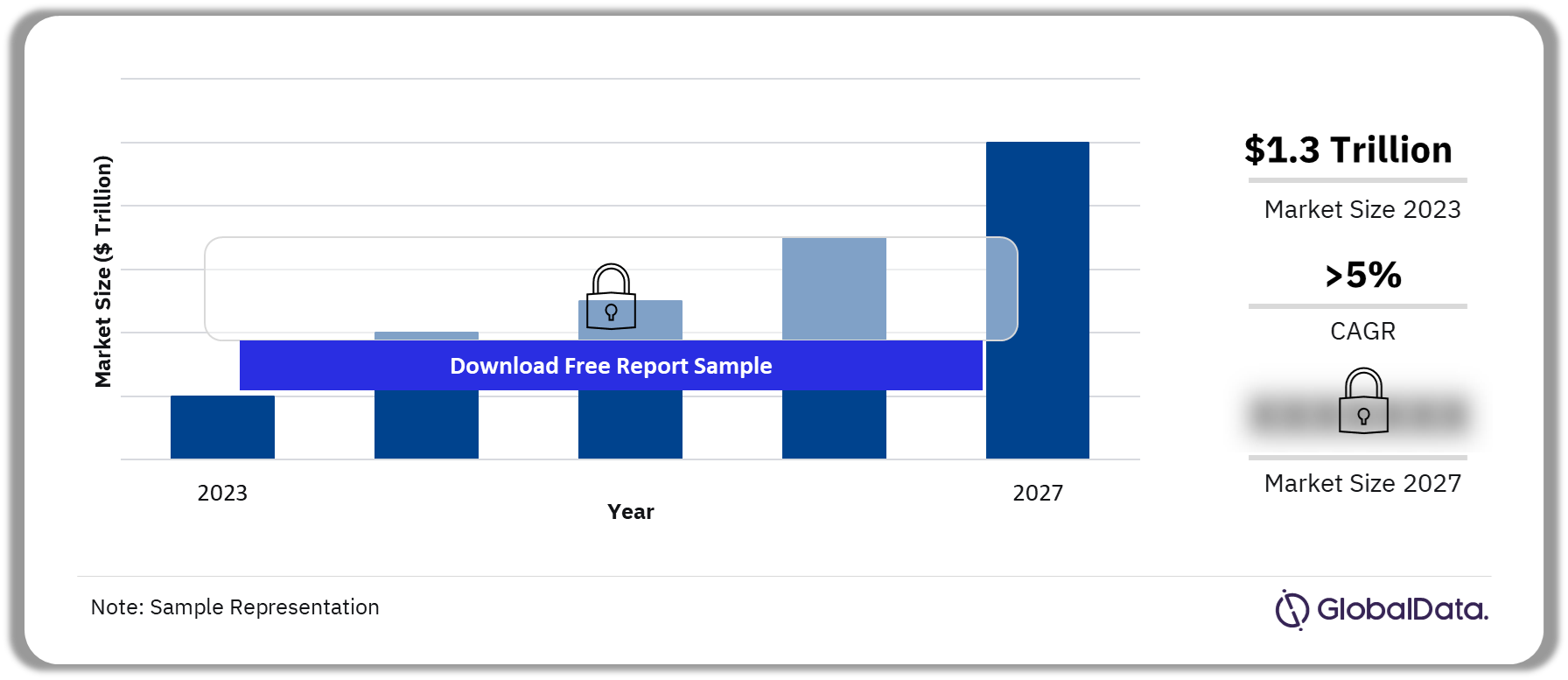

The annual value of card transactions in the UK cards and payments market was $1.3 trillion in 2023. The value is expected to grow at a CAGR of more than 5% during 2023-2027. Fintech companies are offering international P2P payment platforms to cater to the rising demand for cross-border payments. For instance, in March 2023, Brightwell partnered with Visa to enable users to make international money transfers.

UK Card Transactions Outlook, 2023-2027 ($ Trillion)

Buy the Full Report for More Information on the UK Cards and Payments Market Forecast

The UK cards and payments market research report provides a detailed analysis of market trends influencing the industry. It provides transaction values and volumes for several payment instruments for the review period. In addition, the UK cards and payments market analysis offers information on the country’s competitive landscape, including market shares of issuers and schemes. The report also entails regulatory policy details and provides extensive coverage of any recent changes in the regulatory structure.

| Annual Value of Card Transactions (2023) | $1.3 trillion |

| CAGR (2023-2027) | >5% |

| Forecast Period | 2023-2027 |

| Historical Period | 2019-2022 |

| Key Payment Instruments | · Cards

· Cash · Credit Transfers · Mobile Wallets · Direct Debits · Cheques |

| Key Segments | · Card-Based Payments

· Merchant Acquiring · Ecommerce Payments · In store Payments · Buy Now Pay Later |

| Leading Players | · Apple Pay

· Santander · Visa · Barclays · HSBC |

| Enquire & Decide | Discover the perfect solution for your business needs. Enquire now and let us help you make an informed decision before making a purchase. |

UK Cards and Payments Market Dynamics

In the UK, Fintech companies and digital-only banks are entering the payment card space. For instance, in November 2022, a Nigerian digital bank, Kuda that was launched in the UK, is offering services such as fund transfers, saving accounts, and physical and virtual payment cards. In addition, contactless payments are increasingly being rolled out for transport. For instance, recently in September 2023, an UK-based payment company Unicard announced a partnership with Transport for Wales, which will enable commuters to pay for public transport using contactless payment cards and mobile wallets.

Buy the Full Report to Get Additional UK Cards and Payments Market Dynamics

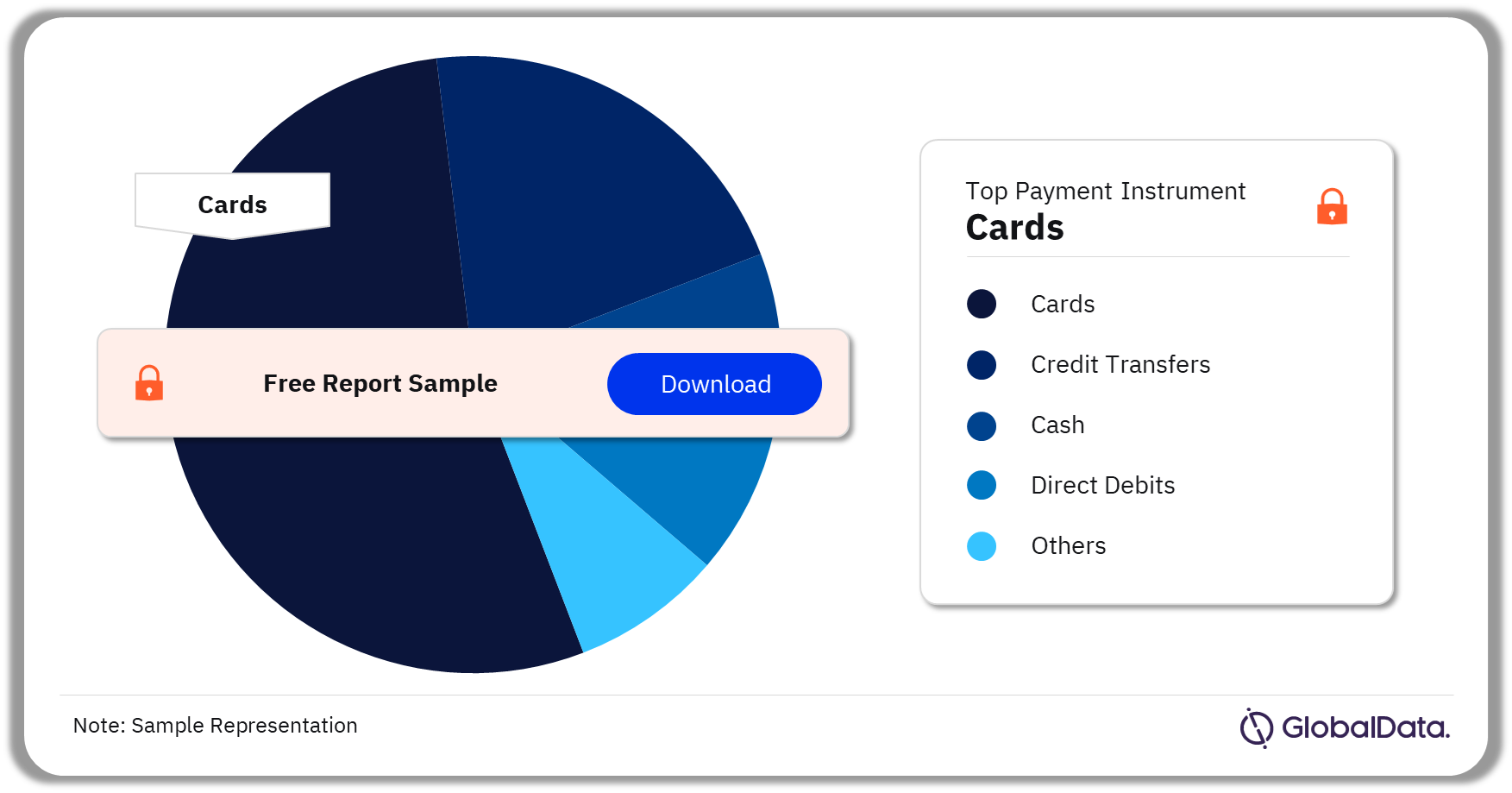

UK Cards and Payments Market Segmentation by Payment Instruments

Cards had the highest share of payment transaction volume in 2023.

The key payment instruments in the UK cards and payments market are cash, mobile wallets, credit transfers, cards, direct debits, and cheques. Cards led the market in 2023 in terms of transaction volume. This is attributed to the convenience of electronic payments, robust payment infrastructure, the increasing preference for contactless payments, and ecommerce market growth.

UK Cards and Payments Market Analysis by Payment Instruments (Volume Terms), 2023 (%)

Buy the Full Report for More Payment Instrument Insights into the UK Cards and Payments Market

UK Cards and Payments Market Segments

Apple Pay is the most popular in ecommerce payments

The key segments in the UK cards and payments market are card-based payments, merchant acquiring, e-commerce payments, in-store payments, and buy now pay later, among others.

Ecommerce Payments: E-commerce in the UK has registered healthy growth in the last few years. This is attributed to the prevalence of smartphones, widespread internet penetration, the availability of secure online payment systems, and the increasing number of online shoppers. The popularity of online shopping events such as Black Friday and Cyber Monday has also propelled ecommerce growth.

Alternative payment solutions such as Apple Pay, PayPal, and Amazon Pay are also used for online payments. Apple Pay accounted for more than 8% of total ecommerce transaction value in 2023. PayPal is the second most popular alternative payment option.

Buy the Full Report for More Market Segment Insights into the UK Cards and Payments Market

UK Cards and Payments Market - Competitive Landscape

A few of the leading players in the UK cards and payments market are:

- Apple Pay

- Santander

- Visa

- Barclays

- HSBC

Apple Pay: It was launched in the UK in July 2015 to make in-store, in-app, and online payments. Card issuers and schemes that support Apple Pay in the UK include American Express, Mastercard, Visa, Barclays, Barclaycard, First Direct, and Ulster Bank among others.

Leading UK Cards and Payments Players, 2023

Buy the Full Report to Know More about the Leading UK Cards and Payments Companies Download a Free Sample Report

UK Cards and Payments Market – Latest Developments

- In May 2021, UK-based cryptocurrency wallet and payment platform Zumo launched a virtual card offering. The card enables holders to use cryptocurrencies to make purchases at any online retailer that accepts Visa. The card is designed to convert Bitcoin and Ether cryptocurrencies into traditional fiat currencies to enable online transactions.

- In August 2023, US-based auto manufacturer Tesla launched the first V4 Supercharging device with contactless payment functionality.

Segments Covered in the Report

UK Cards and Payments Instruments Outlook (Value, $ Trillion, 2019-2027)

- Cash

- Mobile Wallets

- Credit transfers

- Cards

- Direct debits

- Cheques

UK Cards and Payments Market Segments Outlook (Value, $ Trillion, 2019-2027)

- Card-Based Payments

- Merchant Acquiring

- Ecommerce Payments

- In store Payments

- Buy Now Pay Later

Scope

This report provides:

- Current and forecast values for each market in the UK cards and payments industry, including debit and credit cards.

- Detailed insights into payment instruments, including cards, credit transfers, cheques, and direct debits. It also includes an overview of the country’s key alternative payment instruments.

- E-commerce market analysis.

- Analysis of various market drivers and regulations governing the UK cards and payments industry.

- Detailed analysis of strategies adopted by banks and other institutions to market debit and credit cards.

- Comprehensive analysis of consumer attitudes and buying preferences for cards.

- The competitive landscape of the UK cards and payments industry.

Reasons to Buy

- Make strategic business decisions, using top-level historical and forecast market data, related to the UK cards and payments industry and each market within it.

- Understand the key market trends and growth opportunities in the UK cards and payments industry.

- Assess the competitive dynamics in the UK cards and payments industry.

- Gain insights into marketing strategies used for various card types in the UK.

- Gain insights into key regulations governing the UK cards and payments industry.

NatWest Group

Barclays

HSBC

Santander

Nationwide Building Society

Banco Sabadell

Capital One

Vanquis Bank

Virgin Money

The Co-operative Bank

American Express

Diners Club

Visa

American Express

Table of Contents

Frequently asked questions

-

What was the annual value of card transactions in the UK cards and payments market in 2023?

The annual value of card transactions in the UK cards and payments market was $1.3 trillion in 2023.

-

What is the expected growth rate of the annual card transactions in the UK cards and payments market for the forecast period?

The annual value of card transactions in the UK cards and payments market is expected to grow at a CAGR of more than 5% during 2023-2027.

-

Which was the leading payment instrument in the UK cards and payments market in 2023?

Cards was the leading payment instrument in terms of transaction volume in the UK cards and payments market in 2023.

-

Which are the leading players in the UK cards and payments market?

The leading players in the UK cards and payments market are Apple Pay, Santander, Visa, Barclays, and HSBC, among others.

Get in touch to find out about multi-purchase discounts

reportstore@globaldata.com

Tel +44 20 7947 2745

Every customer’s requirement is unique. With over 220,000 construction projects tracked, we can create a tailored dataset for you based on the types of projects you are looking for. Please get in touch with your specific requirements and we can send you a quote.

Sample Report

United Kingdom (UK) Cards and Payments – Opportunities and Risks to 2027 was curated by the best experts in the industry and we are confident about its unique quality. However, we want you to make the most beneficial decision for your business, so we offer free sample pages to help you:

- Assess the relevance of the report

- Evaluate the quality of the report

- Justify the cost

Download your copy of the sample report and make an informed decision about whether the full report will provide you with the insights and information you need.

Related reports

View more Payments reports