United Kingdom (UK) SME Insurance Market Size, Trends, Competitor Dynamics and Opportunities

Powered by ![]()

All the vital news, analysis, and commentary curated by our industry experts.

UK SME Insurance Competitive Analysis Report Overview

Despite the significant economic challenges faced by small and medium-sized enterprises (SMEs) in recent years, the number of SMEs still increased in the UK in 2023. This growth highlights the importance of these companies as a source of business growth in the commercial insurance sector. Since SME switching behavior has increased, insurers should offer cheaper or more affordable policies.

The UK SME insurance market research report presents information on the leading insurers in the SME segment and examines their methodologies for developing propositions. The report also highlights how competitor positions vary among micro, small, and medium enterprises. Furthermore, it reveals which insurers are winning over brokers and with which companies SMEs are placing their businesses.

| Key Channels | · Brokers

· Direct Channels · Banks · PCW |

| Leading Providers | · Aviva

· AXA · Zurich · Direct Line · NFU Mutual |

| Enquire & Decide | Discover the perfect solution for your business needs. Enquire now and let us help you make an informed decision before making a purchase. |

UK SME Insurance Market Critical Success Factors

- Offering affordability and support to SMEs amid economic challenges: Insurers can support SMEs by customizing policies to meet a range of needs during the UK’s cost-of-living crisis and stagnant economy. However, providing more cost-effective policies became critical as a result of increased switching behavior in 2023.

- Provision of value-added services such as advice on business strategy and marketing support: Offering value-added services such as marketing support and business strategy advice is a growing opportunity for sole traders and micro businesses. In addition, there is an opportunity to provide marketing support to SMEs.

Buy the Full Report for More Critical Success Factors of the UK SME Insurance Market

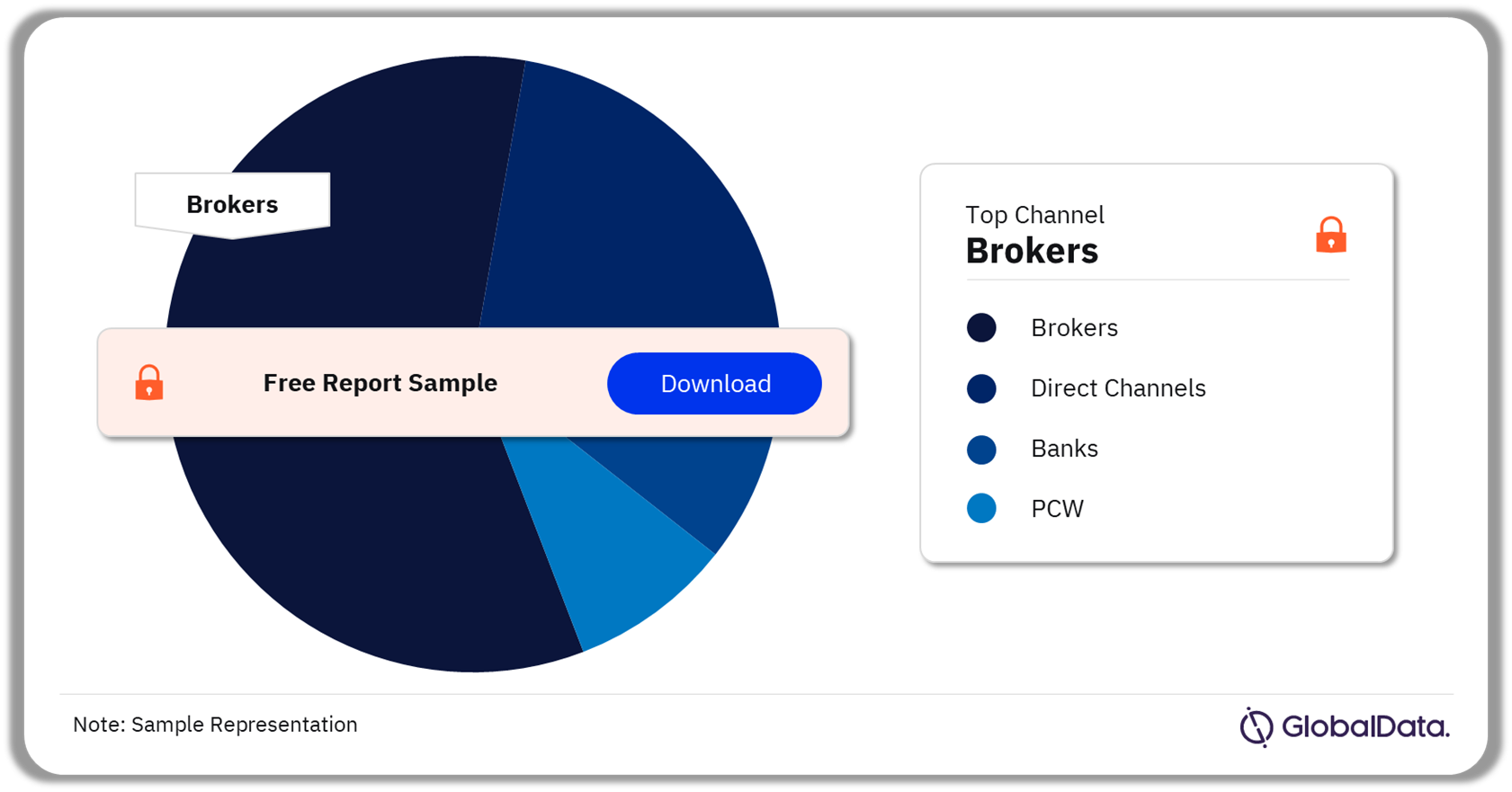

UK SME Insurance Market Segmentation by Channels

Brokers is the most important distribution channel in the SME insurance market

The key channels in the UK SME insurance market are brokers, direct channels, banks, and PCW. Most of the SME insurance policies were sold through brokers in 2023. Insurance brokers are essential to the distribution of commercial insurance. The presence of brokers has a significant impact on the competitive dynamics within the market. Aviva continues to hold a leading position in the packaged and non-packaged insurance markets in the brokers sub-segment.

UK SME Insurance Market Analysis by Channels, 2023 (%)

Buy the Full Report for More Channel Insights into the UK SME Insurance Market

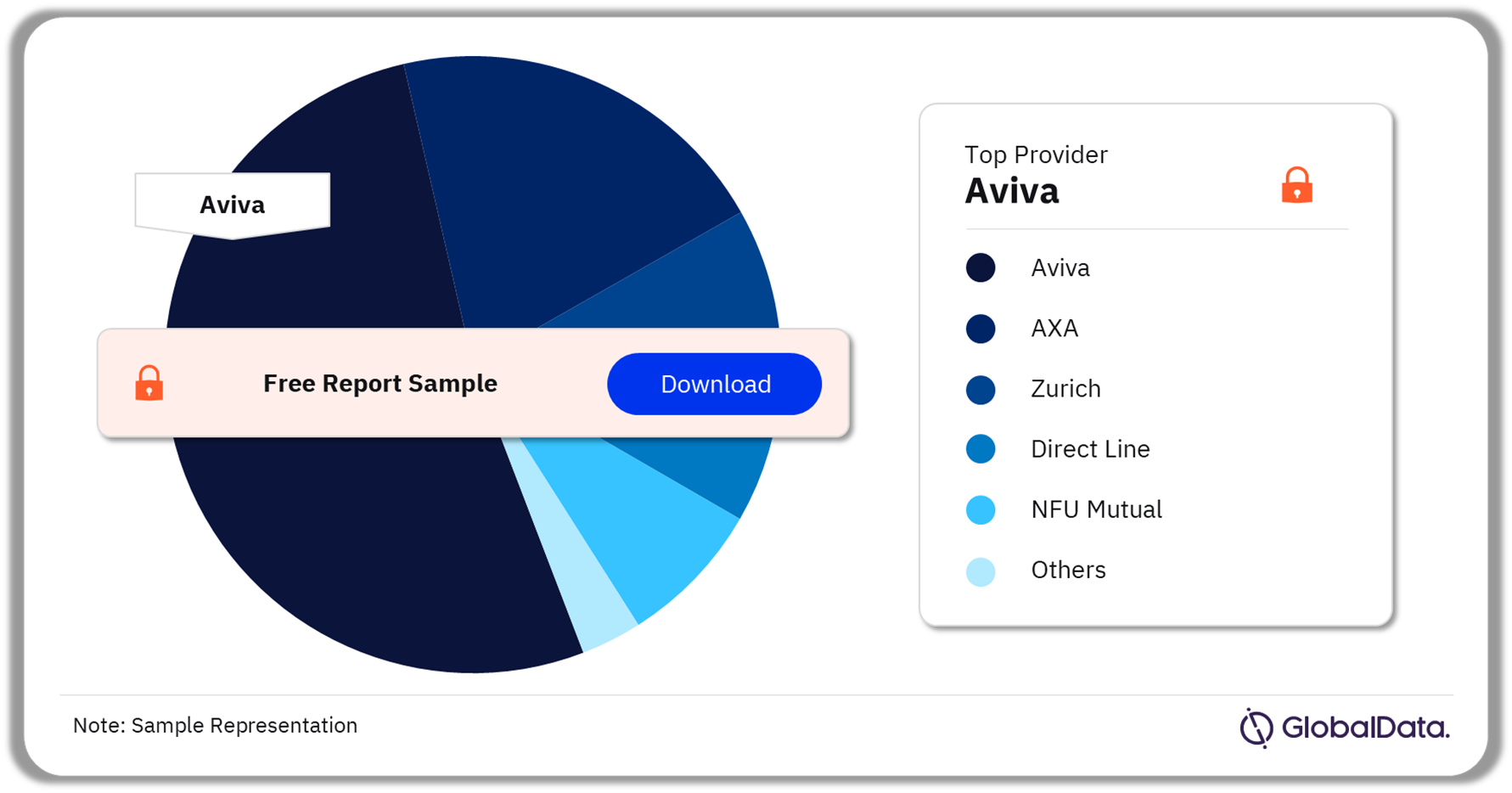

UK SME Insurance Market – Competitive Landscape

Aviva sold the highest number of contracts in 2023

A few of the leading providers in the UK SME insurance market are Aviva, AXA, Zurich, Direct Line, and NFU Mutual. Aviva’s strong performance, particularly in the domain of commercial brokers, influenced competitive conditions within SME insurance. Meanwhile, Barclays and Lloyds Bank dominated the bancassurance market in 2023. Aviva, AXA, and Zurich will continue to dominate the market in 2024 due to their substantial product offerings, strong relationships with commercial brokers, and strong market presence.

UK SME Insurance Market Analysis by Providers, 2023 (%)

Buy the Full Report for More Provider Insights into the UK SME Insurance Market

UK SME Insurance Market - Latest Developments

- A new cyber insurance product designed specifically for micro businesses was launched by Aviva in October 2023. The product is designed to improve access for smaller businesses. It includes several benefits such as credit monitoring, reputation management, and identity fraud monitoring services.

- Zurich UK invested in AI and natural language processing technologies in June 2023 to strengthen its efforts in the fight against claims fraud. The insurer has automated its research and intelligence-gathering procedures in partnership with Xapien, allowing for the quick validation of background data in a matter of minutes.

Segments Covered in the Report

UK SME Insurance Channels Outlook

- Brokers

- Direct Channels

- Banks

- PCW

Scope

- Identify the leading players in the UK SME insurance market.

- Learn about the providers of choice for SME insurance among brokers.

- Discover the strategies and Net Promoter Scores of the top SME insurers.

- Identify growth opportunities in the SME space.

- Find out which value-added services are in demand.

Reasons to Buy

• Identify the leading players in the UK SME insurance market .

• Learn the providers of choice for SME insurance among brokers.

• Discover the strategies and Net Promoter Scores of the top SME insurers.

• Identify growth opportunities in the SME space.

• Find out which value-added services are in demand.

AXA

Direct Line

Lloyds Bank

Barclays

Zurich

LV=

NFU Mutual

Bupa

Simply Business

NIG

RSA

Bank of Scotland

RBS

HSBC

Santander

NatWest

Xapien

Hiscox

Table of Contents

Table

Figures

Frequently asked questions

-

What are the key channels in the UK SME insurance market?

The key channels in the UK SME insurance market are brokers, banks, PCW, and direct channels.

-

Which was the leading channel for purchasing SME insurance policies in 2023?

In 2023, the leading channel for purchasing SME insurance policies was through brokers.

-

Which are the leading providers in the UK SME insurance market?

A few of the leading providers in the UK SME insurance market are Aviva, AXA, Zurich, Direct Line, and NFU Mutual.

Get in touch to find out about multi-purchase discounts

reportstore@globaldata.com

Tel +44 20 7947 2745

Every customer’s requirement is unique. With over 220,000 construction projects tracked, we can create a tailored dataset for you based on the types of projects you are looking for. Please get in touch with your specific requirements and we can send you a quote.

Sample Report

United Kingdom (UK) SME Insurance Market Size, Trends, Competitor Dynamics and Opportunities was curated by the best experts in the industry and we are confident about its unique quality. However, we want you to make the most beneficial decision for your business, so we offer free sample pages to help you:

- Assess the relevance of the report

- Evaluate the quality of the report

- Justify the cost

Download your copy of the sample report and make an informed decision about whether the full report will provide you with the insights and information you need.

Related reports

View more Non-Life Insurance reports