United Kingdom (UK) Financial Advisors Market Overview by Financial Advice Firms, Opportunities and Threats, 2023 Update

Powered by ![]()

All the vital news, analysis, and commentary curated by our industry experts.

United Kingdom (UK) Financial Advisors Market Report Overview

The UK financial advisors market is undergoing a period of consolidation, as a result, the composition of the market is changing slowly but surely owing to ready sellers and willing buyers. Single advisor firms still dominate the market. However, the average number of advisors per firm is rising, indicating a shift towards medium-sized and large outfits. Financial advisors play an important role in serving retired individuals and those approaching retirement. However, the enduring challenge lies in closing the advice gap, as less than 10% of consumers have accessed regulated financial advice. The Financial Conduct Authority (FCA) is revisiting this issue with the new Advice Guidance Boundary Review (AGBR); this is likely to be an increasing focus for advisors now that implementation of the Consumer Duty rules is well underway.

The United Kingdom (UK) Financial Advisors market research report discusses the key trends shaping the UK financial advisory market in 2023. It covers the market size and growth forecasts of the financial advisory market in the UK (including profitability), merger and acquisition activity, as well as the key threats and opportunities cited by advisors.

| Key Channels | · Independent Financial Advisors

· Investment Management Companies (Platform Only) · Advisors at Client’s Main Bank · Investment Management Company · Investment Platform at Client’s Main Bank |

| Enquire & Decide | Discover the perfect solution for your business needs. Enquire now and let us help you make an informed decision before making a purchase. |

UK Financial Advisors Market Critical Success Factors

Explore the opportunities offered by generative AI: Generative AI has dominated the media agenda over the last 12 months. While it is still in its nascent stage, the consensus is that generative AI tools will increasingly be used in the world of work. Advisors must explore how the technology can help enhance their productivity, for example, in the area of letter writing and summarizing regulations, as well as training and skills requirements.

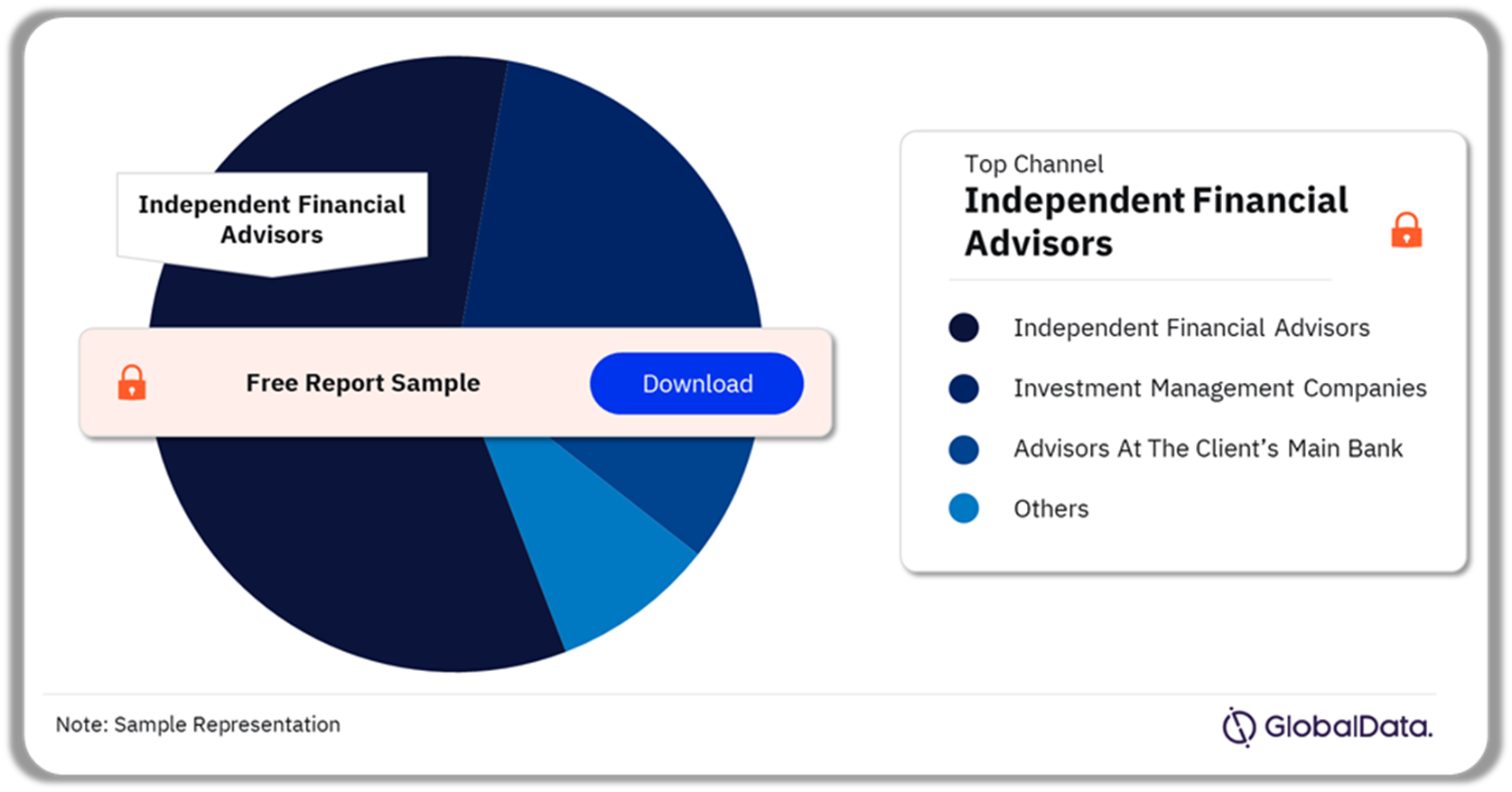

UK Financial Advisors Market Segmentation by Channels

The key channels preferred by the UK financial advisors market are independent financial advisors, investment management companies (platform only), advisors at the client’s main bank, investment management company, and investment platform at the client’s main bank. Among investors, financial advisors are the preferred channel for arranging investments.

In 2023, more than 24% of investors selected financial advisors. It is followed by competing channels such as investment management company platforms and bank-based advisors.

UK Financial Advisors Market Analysis by Channels, 2022 (%)

Buy the Full Report for More Insights on the UK Financial Advisors’ Market Preferred Channels, Download a Free Report Sample

UK Financial Advisors Market Trends

One of the major themes for the UK’s financial advisors is managing their business and advising clients against the difficult macroeconomic backdrop. The 2023 and, to date, 2024 UK financial advisors market have proved comparatively stable after the particularly volatile 2020-2022 period. However, there are still several challenges to contend with. For instance, economic growth is stagnating, the performance of domestic financial markets is lackluster, and a General Election is looming.

In addition to that, there is a heavy regulatory burden to contend with. Consumer Duty continues to be a key theme, although with implementation now well underway attention is turning to new regulatory activity, notably the AGBR. Finally, financial advisors are also investigating the opportunities offered by an aging population, the potential of ESG investing, and how generative AI can bring productivity gains.

Buy the Full Report for More Insights on the UK Financial Advisors Market Trends, Download A Free Report Sample

Segments Covered in the Report

UK Financial Advisors Market Channels Outlook

- Independent Financial Advisors

- Investment Management Companies (Platform Only)

- Advisors at Client’s Main Bank

- Investment Management Company

- Investment Platform at Client’s Main Bank

Scope

- This report discusses the key trends shaping the UK’s financial and investment advice space throughout 2023 and beyond.

- It covers the size and growth of the financial advice market (including profitability), merger and acquisition activity, as well as the key threats and opportunities cited by advisors.

- The report also discusses how market trends such as ESG, artificial intelligence, and regulation will shape the sector in the future.

Reasons to Buy

- Understand the latest data on the size and composition of the UK financial advice market.

- Find out about the latest M&A deals in the consolidating financial advice space.

- Learn who uses financial advisors and what their motivations are for doing so.

- Discover the key trends and themes affecting the financial advice industry.

- Understand the current regulatory challenges that financial advisors are facing.

- Learn more about how advisors can prepare for The Great Wealth Transfer.

- Uncover the opportunities offered by ESG investing and the productivity gains of generative AI.

Fairstone

Wren Sterling

and Skerritts

Lync Wealth Management

Sheafmoor Money Management

North Financial Management

Liberate Wealth

Soderberg & Partners

Canaccord Genuity

Table of Contents

Table

Figures

Frequently asked questions

-

Which advisor firms dominated the market in 2022?

Single advisor firms dominated the market in 2022.

-

Which are the key channels preferred by the UK financial advisors market?

A few of the key channels preferred by the UK financial advisors market are independent financial advisors, investment management companies (platform only), advisors at the client’s main bank, investment management company, and investment platform at the client’s main bank.

-

Which is the most preferred channel for arranging investments for investors?

Among investors, financial advisors are the preferred channel for arranging investments.

Get in touch to find out about multi-purchase discounts

reportstore@globaldata.com

Tel +44 20 7947 2745

Every customer’s requirement is unique. With over 220,000 construction projects tracked, we can create a tailored dataset for you based on the types of projects you are looking for. Please get in touch with your specific requirements and we can send you a quote.

Sample Report

United Kingdom (UK) Financial Advisors Market Overview by Financial Advice Firms, Opportunities and Threats, 2023 Update was curated by the best experts in the industry and we are confident about its unique quality. However, we want you to make the most beneficial decision for your business, so we offer free sample pages to help you:

- Assess the relevance of the report

- Evaluate the quality of the report

- Justify the cost

Download your copy of the sample report and make an informed decision about whether the full report will provide you with the insights and information you need.

Related reports

View more Wealth Management reports